|

|

| My favourite pages |

| Support topics

Need help in something? Take a look at our support area for your answer. Find out more |

|

|

| My favourite pages |

| Support topics

Need help in something? Take a look at our support area for your answer. Find out more |

Session Timeout

You have been inactive for 0 mins.

Stay logged in or you will be logged off in 60 seconds.

Asset Allocation Explained |

Equity – Often referred to as shares. Shares are units of ownership in a company which entitle the holder to certain rights for example to exercise voting rights or to participate in the company’s profits.

Fixed Income – Often referred to as fixed interest or bonds. When you invest in bonds, you are typically lending money to a company or a government in return for a defined series of interest payments and the promise that a defined value (called the ‘face’ or ‘par’ value) will be returned at a certain point in time

Property – Investments in property include residential, offices, warehouses and shopping centres.

Cash – Money held in cash or cash-like instruments, often to ensure there are sufficient liquid assets within a portfolio.

Other – Contains other investments such as commodities, preferred stock and derivatives.

Portfolio Risk Explained |

Investing involves risk, but there are many types of 'risk' so it's important to be clear about what it really means for you and your money. When investors talk about risk they're often thinking about things like getting disappointing returns, losing money, failing to keep pace with the cost of living or missing out on a specific goal.

What we're really talking about here is uncertainty. It's hard to measure, but one approach is to look at the volatility of the investments in your portfolio – how much they have tended to fluctuate in value. The more risk you take with your investments, the higher the rewards might be, but the potential to lose money also increases. Too much risk might be expensive and stressful to live with, but too little could mean your investments don't keep pace with inflation and lose their buying power over time.

The key is to find the level that's right for you – the level that you're comfortable with and able to cover financially. Finding it depends on a number of things

Measuring the level of risk in an investment portfolio is difficult. Risk measurement methods use mathematical tools and techniques and are based on a number of assumptions, often based on how an investment has performed in the past. As we know however, what's happened in the past isn't necessarily a good predictor of what might happen in the future so this should always be borne in mind when using portfolio risk measures.

Despite their limitations, with a proper understanding of how they should be interpreted, risk measures can be a useful tool in the investment decision making process. They should always be regarded as useful indicators and nothing more – to help inform your investing decisions but not to drive them in their entirety.

Equity Styles Explained |

Market capitalisation is an indication of the size of the companies being invested in. It is calculated by multiplying the number of shares issued by the company by the current share price. Market capitalisation is divided into ‘large’, ‘medium’ or ‘small’ according to the below:

Large – Companies that have a market capitalisation greater than $10 billion.

Medium – Companies that have a market capitalisation between $2 billion and $10 billion.

Small – Companies that have a market capitalisation below $2 billion.

Companies can be categorised as ‘value’, ‘blend’ or ‘growth’ as defined below:

Value – Companies that are considered to be trading at a share price below what their fundamentals would suggest.

Blend – Companies that do not exhibit solely value or growth characteristics.

Growth – Typically well-established companies which are considered to have above average prospects for long-term growth.

Equity Regions Explained |

Equity region indicates in which countries the underlying shares within your portfolio are listed.

USA – Companies listed on a stock market in the USA.Canada – Companies listed on a stock market in Canada.

Latin America – Companies listed on stock markets in the Caribbean, Central America and South America, such as Mexico, Brazil and Argentina.

United Kingdom – Companies listed on a stock market in the United Kingdom, Guernsey, Isle of Man and Jersey.

Eurozone – Companies listed on stock markets in countries which have the Euro as their official currency, such as France, Germany and Spain.

Europe ex Eurozone – Companies listed on stock markets in western European countries which do not have the Euro as their official currency, such as Denmark, Sweden and Switzerland.

Europe Emerging – Companies listed on stock markets in European emerging markets, such as Poland, Russia and Turkey.

Africa – Companies listed on stock markets in African countries, such as Egypt, Nigeria and South Africa.

Middle East – Companies listed on stock markets in Middle Eastern countries, such as Israel, Qatar and Saudi Arabia.

Japan – Companies listed on a stock market in Japan.

Australasia – Companies listed on stock markets in Australia and New Zealand.

Asia Developed – Companies listed on stock markets in developed Asian countries, such as Hong Kong, Singapore and Taiwan.

Asia Emerging – Companies listed on stock markets in emerging Asian countries, such as China, India and Thailand.

Equity Sectors Explained |

Cyclical – Companies which operate in industries that are considered to be significantly affected by economic shifts. When the economy is prosperous, these industries tend to expand and when the economy is in a downturn they tend to shrink.

Basic Materials - Companies that manufacture chemicals, building materials and paper products. This sector also includes companies engaged in commodities exploration and processing.

Consumer Cyclical - This sector includes retail stores, auto and auto-parts manufacturers, restaurants, lodging facilities, specialty retail and travel companies.

Financial Services - Companies that provide financial services include banks, savings and loans, asset management companies, credit services, investment brokerage firms and insurance companies.

Real Estate - This sector includes companies that develop, acquire, manage and operate real estate properties.

Sensitive – Companies that operate in industries that ebb and flow with the overall economy, but not severely. Sensitive industries fall between defensive and cyclical, as they are not immune to a poor economy, but they also may not be as severely affected as cyclicals.

Communication Services - Companies that provide communication services using fixed-line networks or those that provide wireless access and services. Also includes companies that provide advertising & marketing services, entertainment content and services, as well as interactive media and content provider over internet or through software.

Energy - Companies that produce or refine oil and gas, oilfield-services and equipment companies and pipeline operators. This sector also includes companies that mine thermal coal and Uranium.

Industrials - Companies that manufacture machinery, hand-held tools and industrial products. This sector also includes aerospace and defence firms as well as companies engaged in transportation services.

Technology - Companies engaged in the design, development and support of computer operating systems and applications. This sector also includes companies that make computer equipment, data storage products, networking products, semiconductors and components.

Defensive – Companies which operate in industries that are relatively immune from economic shifts. These industries provide services that consumers require in both good and bad times.

Consumer Defensive – Companies that manufacture food, beverages, household and personal products, packaging, or tobacco. Also includes companies that provide services such as education and training services.

Healthcare – This sector includes biotechnology, pharmaceuticals, research services, home healthcare, hospitals, long-term-care facilities and medical equipment and supplies. Also includes pharmaceutical retailers and companies which provide health information services.

Utilities - Electric, gas and water utilities.

Product Involvement Explained |

Product Involvement metrics measure the percentage of a portfolio's assets exposed to a range of business areas and activities. For example, if a fund's involvement in Animal Testing is 20%, that means 20% of the fund's assets are invested in companies involved in Animal Testing.

Exposure percentages are calculated by summing the weights of a portfolio’s holdings in the companies involved in each area. In most cases a company is considered ‘involved’ in a certain area if it's revenue from that area exceeds a certain minimum threshold. In other areas, for example animal testing, abortion, contraceptives and human embryonic stem cell research, there is no revenue threshold such that if the company has any involvement at all in these areas, it will be considered involved. If a company is considered involved in an area, the entire weight of that company in a portfolio is counted when determining the overall percentages shown.

|

|

ESG Pillars Explained |

Morningstar's ESG Pillar Scores help investors understand how a fund is performing in three key areas: Environmental (E), Social (S), and Governance (G). These scores break down the overall sustainability risk of a portfolio into these specific categories.

Each score reflects how much environmental, social, and governance factors contribute to the overall risk of companies in the fund. The scores are averaged based on the size of each company in the portfolio. Lower scores mean lower risk.

To receive these scores, at least 67% of the fund’s assets must be rated for their ESG risk. This provides investors with a clearer view of a fund’s exposure to sustainability risks in different areas.

These are domiciled outside the UK but have been given recognised status by the Financial Conduct Authority (FCA) and can be held in any of our investment accounts.

Overseas funds can be recognised by the FCA if they meet certain requirements (under section 272 of the Financial Services and Markets Act 2000).

The term (recognised funds) also refers to funds domiciled within in the European Economic Area which are in one of the transitionary arrangements created following Brexit, namely the Overseas Funds Regime (OFR) or the Temporary Marketing Permissions Regime (TMPR).

The FCA is currently in the process of moving European funds from the TMPR to the OFR. This process is expected to continue until the end of 2026.

A fund which is domiciled overseas must have one form of FCA recognition for it to be sold to UK investors.

An overseas domiciled fund which has FCA recognised status can be sold to UK investors. Unlike regulated UK domiciled funds however, such a fund may not fall under the remit of the UK Financial Services Compensation Scheme (FSCS) or the UK Financial Ombudsman Service – please see our dedicated money protection page for further information.

Therefore, complaints and compensation arrangements lay within the jurisdiction of where the funds are domiciled (e.g. Luxembourg, Dublin etc). These will generally be different to those available for UK based funds.

A large proportion of overseas domiciled funds are based in either Luxembourg or Dublin. Of those domiciled in Luxembourg most are held under a SICAV (which is a French acronym for 'Société d’Investissement a Capital Variable') umbrella structure. In much the same way UK funds can be held under an Open Ended Investment Companies (OEIC) umbrella structure. By umbrella structure, we mean a collective investment scheme that exists as a single umbrella entity, under which many sub-funds are held.

For example one umbrella SICAV/OEIC may hold a sub-fund called ‘UK Smaller Companies’ and another sub-fund called ‘UK Equity Income’. Each sub-fund has its own investment aims and is held separately from other sub-funds within the same umbrella. The umbrella structure is often used as it can help to reduce costs for both investors and fund managers.

The FCA recognised status can be applied to either individual funds or to the umbrella structure itself, in which case all funds listed within that structure would have FCA recognised status.

Dublin domiciled funds are generally OEICs.

Investing offshore may offer you a wider choice of funds and the opportunity to diversify your investment portfolio further.

It is important to be aware however, that an investment in an Offshore Fund may:

It is also important not to confuse funds which invest in overseas assets with funds that are based or ‘domiciled’ overseas.

There are many funds based in the UK which provide exposure to different geographical regions. If this is what you are looking for simply filter our ‘find funds’ list by the ‘sector’ which you are interested in (but don’t forget to check the product literature).

In order to determine where an investment is based you might need to dig a little deeper. The following rules of thumb may help:

One easy way to check, where an investment is domiciled is to look at the fund’s factsheet (available for all funds in our ‘find funds’ area) or to look at the provider documentation.

The relevant information is available within the Product Provider’s literature, typically within the main Prospectus, Factsheet or the Key Investor Information Document (KIID).

Funds which have been approved under the OFR are now required to explain, in the fund’s Prospectus or an Appendix to it, whether the fund is eligible for FSCS or FOS coverage.

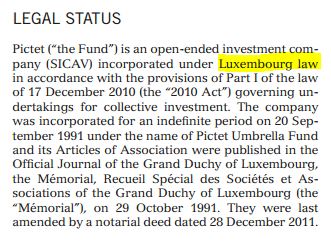

You can view a fund prospectus and any supplementary information via the documents section of the relevant fund factsheet. The fund factsheet can be accessed from our ‘Find Investments’ area and you’ll find information on the fund’s domicile under the ‘Fund Management’ heading, for example:

To offer another example, this is some detail from the Prospectus of a TMPR Fund Provider, showing that the fund is domiciled in Luxembourg:

The best way to check the recognised status of an Offshore domiciled Fund is to visit the Financial Services Register for collective investment schemes and input the relevant Fund details into the fields presented.

Due to the ongoing transition to the OFR which is likely to continue into 2026, we expect that the availability of information about FSCS and FOS protections will improve (in product literature) over the coming years.